SCOTT L. OLSON: Asset Protection For Doctors Made Easy

By Scott L. Olson // August 23, 2015

Protection from creditors and probate, safety, security, diversification, guaranteed income for life, and guaranteed death benefit.

What investment offers 100% protection from creditors (lawsuits)? What investment also offers (1,2) guaranteed income for life; guaranteed increases in future income; guaranteed increase in death benefit; unlimited growth potential, while locking-in gains, for future income for life, and spouse’s life? (3)

Perhaps the most popular financial product for asset-protection planning in Florida is annuities. In Florida annuities are exempt from creditors (4,5).

You could have $100 million in annuities in Florida and have 100% protection from creditors. Florida also offers State Guarantee Protection of up to $100,000 of annuity value and $300,000 of death benefit (6).

Annuity Owners In Good Company

Ben Bernanke’s largest investments are variable annuities (7). Alan Greenspan receives a $3,000 monthly annuity income check (8). The Obama administration proposed special benefits for retirement plan investors who invest in annuities offering guaranteed-income-for-life (9). The U.S. Treasury encourages annuities, which allow for retirees to receive a steady stream of income for the duration of their lifetimes (10).

O.J. Simpson’s advisors put his life savings into annuities and had him move to Florida, because annuities offer unlimited protection from creditors (11). Many annuity investors on the wrong side of nasty law suits were relieved to find their annuities were 100% protected from creditors, while unfortunately their other investments were not.

Even with brilliant advisors, if you don’t own annuities or haven’t spent tens of thousands for irrevocable trusts, you could lose your life savings to lawsuits.

Why Do Wealthy Investors Buy Annuities?

Studies show the biggest fear of the wealthy is running out of income (12). Fixed and Variable annuities offer many guaranteed-income-for-life options.

According to MarketWatch.com, millionaires with $1 to $5 million net-worth’s own 22% of all variable annuities and 20% of all fixed annuities (13). Taxpayers with $100,000 to $1 million in assets own 15% of all variable annuities and 17% of all fixed annuities.

Fixed, Indexed or so-called “so-called Hybrid” annuities do not offer the growth potential of variable annuities.

At least one variable annuity is designed specifically to be owned in trusts to reduce trust income-tax.

Trust tax rates climb to the maximum rate of 39% at only $12,300 of trust income, which could be deferred for generations with the right annuity.

LIMRA estimates investors will buy about $128 Billion of variable annuities with about $45 Billion into fixed indexed annuities in 2015. All annuities combined, average about $235 billion in annual investments (14).

Here are a few benefits of annuities not offered by other investments (1,2)

• Guaranteed Income for Life – even if annuity value falls to zero,

• Creditor Protection – if you get sued you can’t lose your annuity (2,4,5),

• Guaranteed Increases in your future income,

• Tax-Deferral – can help reduce income-tax on social security and Medicare Part B premiums,

• Control of when, and how much income you want,

• Tax-free fund exchanges,

• Free from Probate – pass directly to beneficiaries at death without the cost, delays and publicity of Probate,

• Safety – Backed 100% by issuing companies,

• Liquidity – offer 10-12% annual free withdrawals, and a few variable annuities offer immediate liquidity,

• Annuitization can eliminate need for RMDs,

• Long-Term Care riders (1,2),

• Backed by state insurance departments (6).

Annuities are less expensive than not having guarantees in a market crash.

Annuities Guarantees come with a cost (2), but what’s more expensive – paying a few percent annual fee to guarantee your income for life, and your spouse’s life, with a death benefit for heirs; or not paying the fee and possibly losing half, or more, of your life savings like in the last two crashes?

Why do so many investors at all income levels and risk categories buy annuities?

While the main reason many investor’s choose variable annuities may be the Guaranteed-Income-for-Life, or the Guaranteed-Minimum-Death-Benefit, which granted could be worth a lot, but when it comes to investment performance don’t tune out stellar returns of some VA’s.

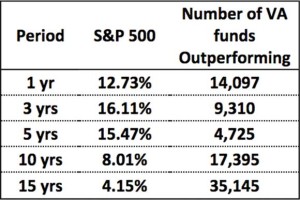

A Few Variable Annuities Offer Great Performance

According to Morningstar there are thousands of VA subaccounts which have outperformed the S&P500 stock market index (15).

According to Morningstar there are thousands of VA subaccounts which have outperformed the S&P500 stock market index (15).

There are 2,184 VA funds which have beat the S&P500 over all time periods. There are 84 VA separate accounts that have doubled the S&P 500’s 15.47% over 5 years – while offering the ability to lock-in profits and the guaranteed income.

Of course the fees for the guarantees, and locked-in benefits reduce these returns by a percent or more annually, but not enough to negate their value.

Fixed Annuities Don’t Pay High Enough Income?

Really? A Florida client is getting 26.14% guaranteed income for life (NOT a typo) with an “Income Annuity” (aka, SPIA, or Pension Annuity). A famous retired attorney is receiving income of 18.86%, guaranteed for as long as he lives.

Many annuity owners, depending on age, are receiving income of 15% or more, mostly tax-free and guaranteed for life.

The older you are, the more you get.

A 91 year old (my father) recently wanted a SAFE INVESTMENT paying him higher income than the bank. His annuity is paying him 19.12% income, paid monthly, mostly tax-free, and guaranteed for life, with no stock-market risk.

Above returns for illustrative purposes and will vary depending on costs of any riders purchased. Past performance does not guarantee future results.

Don’t buy any annuity without getting professional, experienced advice from someone with decades of practical experience, and one who is NOT an “agent” of one company – they may be biased.

Notes: (1) Backed by claims paying ability; (2) Optional benefits available for additional fee; (3) Only with variable annuity sub-accounts; (4) Florida Statute 222.13; (5) assuming annuity is set-up properly; (6 ) Florida Office of Insurance Regulation; (7) Bloomberg.com; (8) FMCCenter.org; (9) NYtimes.com; (10) Treasury.gov; (11) FLProbateLaw.com; (12) Forbes.com; (13) Marketwatch.com; (14) Limra.com; (15) MorningStarAdvisor.com

ABOUT SCOTT L. OLSON

With 37 years’ experience in Financial and Estate-Planning, Wealth Preservation and Wealth Transfer, Scott has been a popular speaker to groups of Attorneys, CPAs, Financial and Estate Planning professionals. He provides Continuing Education courses to Attorneys, and CPAs and has presented to the Florida Bar Tax-Section.

This is not an offer to sell any security or insurance product. Variable annuities are only offered by prospectus. For educational purposes only and NOT an offer to sell any security or insurance product and is NOT an endorsement of any specific Alternative Asset. This information is based on sources we believe reliable but is not considered all-inclusive.

For questions or more information call 321-751-5599.